The Mathematics of Financial Modeling and Investment Management by Sergio M. Focardi, Frank J. Fabozzi, and Petter N. Kolm is an authoritative and in-depth guide to the mathematical techniques that underpin modern financial modeling and investment management. The book serves as a comprehensive resource for finance professionals, academics, and anyone interested in understanding the quantitative foundations of financial decision-making.

Key Features:

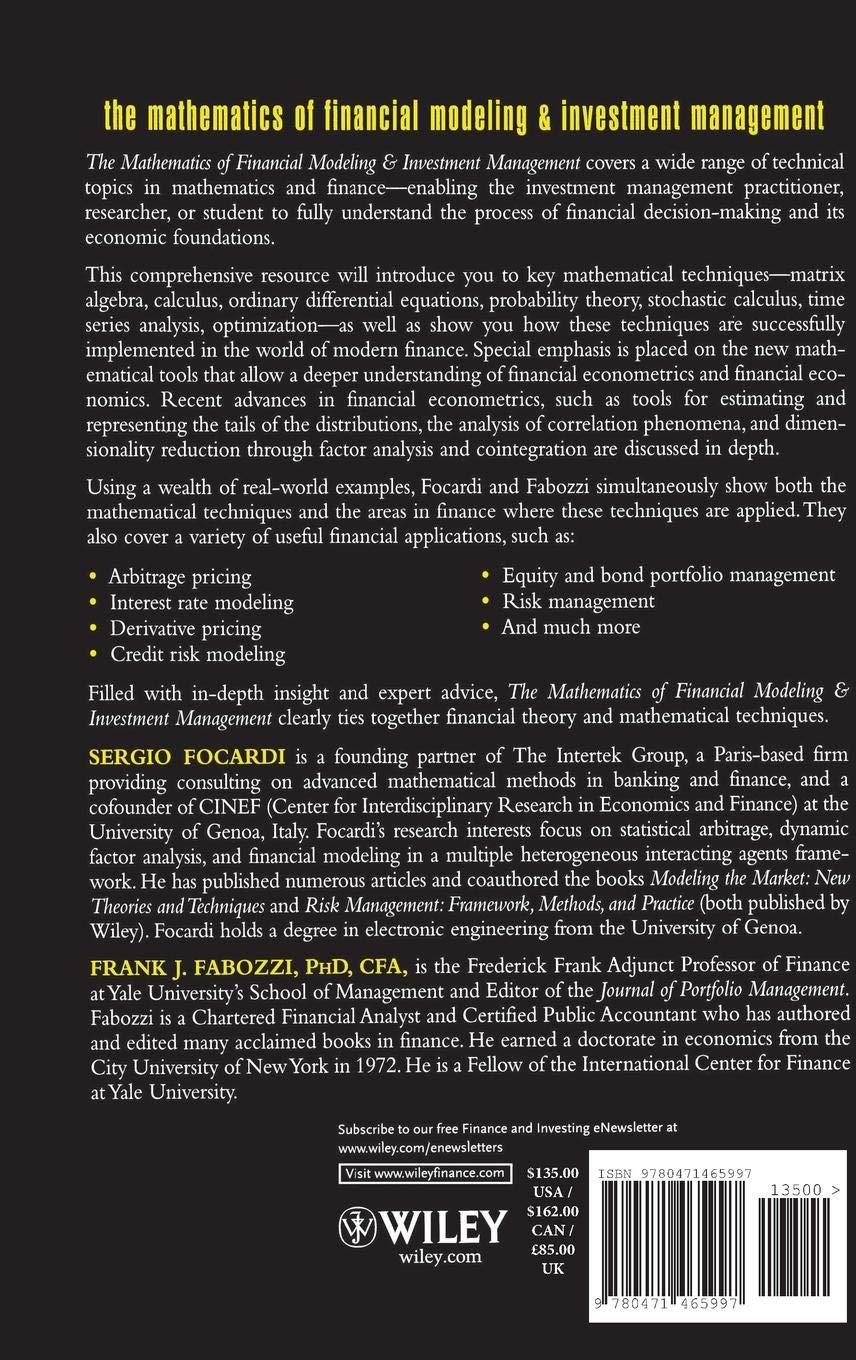

Comprehensive Coverage: The book covers a broad spectrum of topics related to financial modeling and investment management. It provides detailed explanations of the mathematical models used to evaluate and manage investment portfolios, asset pricing, risk management, and performance evaluation. The authors incorporate both theoretical insights and practical applications to help readers understand how to use these tools in real-world financial scenarios.

Mathematical Foundations: Focardi, Fabozzi, and Kolm emphasize the essential mathematical concepts behind the models used in finance. They explain complex topics such as optimization, stochastic processes, time-series analysis, and Monte Carlo simulations, which are all integral to making data-driven decisions in the financial markets.

Portfolio Theory and Asset Pricing: The book offers a deep dive into modern portfolio theory, focusing on techniques for optimizing portfolios, asset allocation, and the trade-off between risk and return. It also explores the principles of asset pricing, providing a thorough understanding of models such as the Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT).

Risk Management and Quantitative Techniques: A significant portion of the book is dedicated to risk management, a critical area for investment professionals. The authors explain how to measure and manage various forms of financial risk, including market risk, credit risk, and operational risk. They also introduce advanced quantitative methods used to model and assess these risks, helping practitioners build more resilient investment strategies.

Practical Applications: Each chapter of the book includes practical examples, case studies, and applications of mathematical models in real-world investment scenarios. These examples help readers understand how to implement complex financial theories and strategies in practice, making the content accessible to both seasoned professionals and newcomers to financial modeling.

Advanced Mathematical Techniques: The book does not shy away from complex mathematical techniques but ensures they are explained in a clear and accessible manner. Topics like stochastic calculus, differential equations, and time-series modeling are broken down step-by-step, enabling readers to apply them effectively in financial contexts.

Statistical Tools and Computation: In addition to theoretical discussions, the authors incorporate a focus on statistical tools and computational methods. This includes practical guidance on how to use these tools for data analysis, forecasting, and modeling financial instruments. The book encourages the use of software tools like MATLAB, R, and Python for performing quantitative analysis.

Investment Strategy and Performance Evaluation: Finally, the book addresses how to use mathematical models to develop robust investment strategies and evaluate the performance of investment portfolios. The authors explore methods for performance measurement, risk-adjusted returns, and benchmarking, ensuring that financial professionals have the tools they need to assess the effectiveness of their investment decisions.

Target Audience:

This book is ideal for finance professionals, portfolio managers, quantitative analysts, and students of finance who want to gain a deeper understanding of the mathematical techniques that drive modern financial modeling and investment management. It is particularly valuable for individuals working in asset management, hedge funds, investment banks, or any financial institution that relies on sophisticated quantitative models for decision-making.

Conclusion:

The Mathematics of Financial Modeling and Investment Management is an essential resource for anyone looking to deepen their understanding of the mathematical principles that form the foundation of financial theory and practice. Whether you are looking to build more efficient investment portfolios, manage risk more effectively, or simply enhance your understanding of the quantitative side of finance, this book provides the knowledge and tools to excel in the dynamic world of financial modeling and investment management.

Reviews

There are no reviews yet.